Share

Historically, per capita healthcare spend by Asian countries has been minuscule compared to that of mega-spenders like the U.S. or Norway. However, with an aging population, rising affluence, and demand for better health services in Asia, healthcare expenditure growth in the APAC region is set to outstrip North America’s. Healthcare spending in Asia is expected to grow at a compounded annual growth rate of 9.2% in the near term, compared to 5.6% in the U.S.

In fact, growth of healthcare spending in many APAC countries has exceeded economic growth over the past few years, resulting in an increasing share of the economy being devoted to health. Between 2000 and 2012, per capita spending on health in Asia grew on average at ~5.6% in real terms, while GDP growth was at ~4.3%.

Despite the substantial growth already taking place in the Asian healthcare industry, a lion’s share of M&A activity is still happening in the U.S., and only ~20% of global healthcare M&A activities in 2012–2013 were transacted in Asia. 2014 was a record year for healthcare M&A activity worldwide — nearly 2,500 deals took place at a total value of ~$412B. Once again, the U.S. dominated with ~66% of that activity being attributable to U.S. domestic deals.

There are several reasons why investors may still be hesitant to focus on Asia — companies are relatively small and may not be in the right stage of growth, diligence is harder to perform, and politics and bureaucracy create barriers. However, there is much profit to be had for those who truly understand market needs and are willing to explore a variety of investment avenues, such as joint ventures or public-private partnerships.

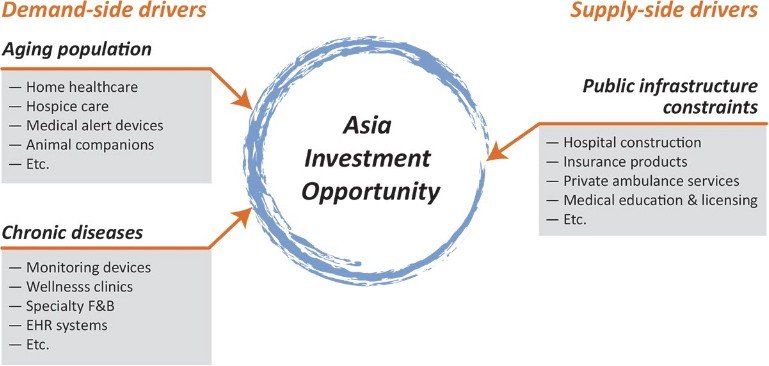

Demand Drivers

Asia’s population is rapidly aging — boosting the need for services such as home health and hospice care, which are increasingly being demanded by this segment.

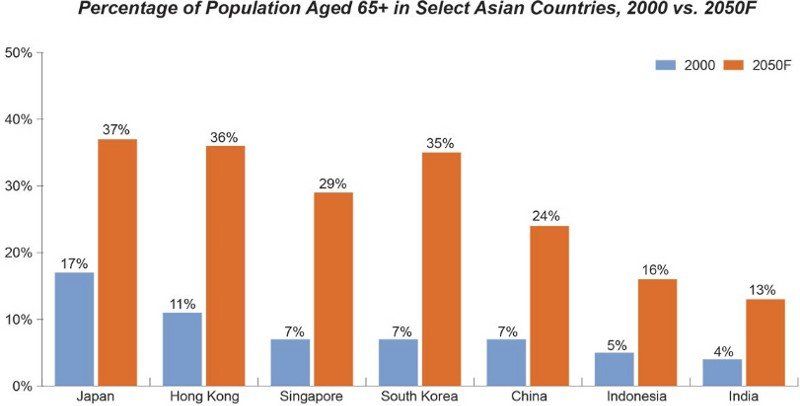

The APAC region is currently home to ~300M people aged 65 or above — over half of the world’s total senior population. This number is growing rapidly due to improvements in life expectancy. As a result, Asia’s aging population is expected to reach~565M by 2030.

Japan is home to the fastest-aging population in the world, with almost a quarter of its population being over the age of 65 — far more than in the U.S. and Europe. Hong Kong, China, Thailand, the Republic of Korea, and Singapore are also seeing a rise in their elderly populations. This trend will accelerate demand for healthcare products and services catered specifically to the 65+ segment.

Many elderly patients prefer to be at home with their loved ones and are willing to pay for the convenience of home healthcare services. The global market for home healthcare is expected to grow at a CAGR of 7.8% to reach ~$355B by 2020, with the APAC region expected to grow fastest at a CAGR of 9.7%. However, there have been just two home health and hospice related deals in Asia in the last two years, compared to 58 in the U.S. over the same period.

A few fast-moving home healthcare providers in the U.S. have identified the gap in Asia and have already started to enter the space. For instance, in 2013, U.S.–based home healthcare firm Bayada purchased a 26% stake in Chennai–based India Home Health Care. This is the first investment outside the U.S. for privately held Bayada.

UN, World Bank, OECD, IMF, IPSS Japan, 2013.

Similar to the home health space, other products and services specifically for the elderly living alone — such as ambulance services, medical alert devices/Personal Emergency Response Systems (PERS), and animal companions — will also see growth. For instance, the global PERS space is set to reach ~$2B by 2020, with ~30% of that market value being derived from Asia.

Asia is expected to be home to half of the global burden of chronic conditions by 2030 — a significant portion of the population that will require specialty care.

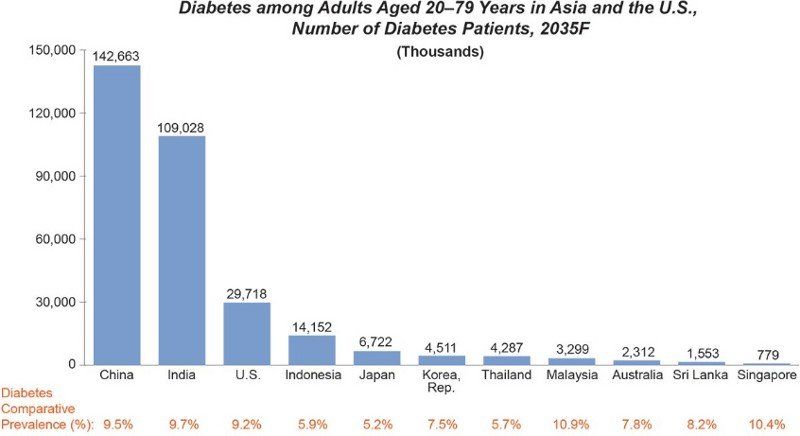

Chronic diseases are the leading cause of mortality in the world — representing 63% of all deaths — and are growing faster in Asia than globally. In 2013, diabetes caused about 5M deaths worldwide, and over 60% of them occurred in the APAC region. The growing prevalence of diabetes and other chronic diseases — such as coronary heart disease and cancer — has created a need for specialty care facilities, wellness plans, healthy products, and health tracking/measuring devices.

The APAC region is currently home to ~215M people who live with diabetes, and this number is expected to reach ~366M by 2030. Projections of significant growth within the region have spurred international players to pursue acquisitions and greenfield projects. For instance, KKR recently completed its biggest buyout in Japan to date by acquiring an 80% stake in Panasonic Healthcare — a provider of digital medical-record systems and instruments that measure blood glucose.

With the increasing need to keep track of chronic disease data, Big Data analytics is also gaining momentum in the Asian healthcare industry, and specialized companies are already making use of this opportunity. For example, U.S.–based Truven Health Analytics, a provider of healthcare data analytics solutions and services, announced the opening of a Singapore-based regional head office to cater to the exponential adoption of patient and clinical data management technology in Asia.

IDF, 2013

Furthermore, there is an increasing demand for wellness products in Asia — in 2013, of the top 10 fastest-growing markets for health and wellness packaged food, five were APAC countries. China, Indonesia, Vietnam, Thailand, and India are significant growth markets that may be of interest to potential investors.

Supply Constraints

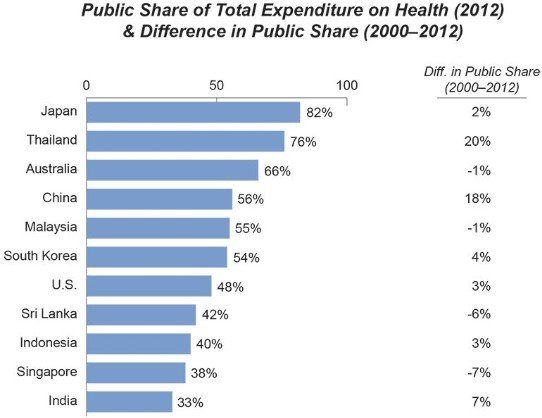

Although governments remain the main financier of healthcare in Asia, public budgetary constraints mean that more private sector participation will be necessary to meet demand.

Governments in Asia, on average, finance ~48 % of total healthcare expenditure in the region (about the same percentage as U.S. public expenditures). This share has increased at a CAGR of just 0.7% in Asia since 2000, resulting in a significant role for the private sector in catering to the rapidly rising growth in demand.

At 3.3 per 1,000 persons, the number of hospital beds in Asia is lower than the OECD average of 4.8, but with significant differences between countries — ranging from 13 beds per 1,000 population in Japan to 0.5 per 1,000 population in the Philippines. Private hospitals in the region are growing, however, and favorable government policies in several countries are also encouraging investments in state hospitals and public-private partnerships.

For example, Seattle-based Columbia Pacific Management Inc. is investing up to $200M to construct two 250-bed multi-specialty hospitals in China. The investment came after China lifted restrictions on foreign-owned hospitals to improve healthcare and address the medical needs of a wealthier, aging population. Chinese authorities in 2014 set up a pilot program that allowed foreign investors in some parts of the country to set up hospitals or acquire existing ones.

Also, in pursuit of lower-cost, higher-profit care options, providers in Asia are expanding outside of the traditional acute hospital setting into outpatient clinics and standalone surgery centers. Each of these areas, and more, represents possible growth and investment opportunities.

Even with rising wages, healthcare is still expensive — especially since many Asian countries lack a

Even with rising wages, healthcare is still expensive — especially since many Asian countries lack adequate health insurance plans. High medical costs coupled with low penetration rates of public insurance open up an opportunity for private insurance companies such as Cigna Corporation, which recently entered into a joint venture with Indian conglomerate TTK Group to sell health insurance products in India.

Conclusion

The trifecta of rapid growth in demand, inadequate supply, and low deal activity makes Asia an ideal target for healthcare investors. As always, the devil is in the details, however — carefully screening these highly varied Asian markets for specific strategic growth opportunities will be vital for those wishing to capitalize on the massive healthcare investment potential in Asia.

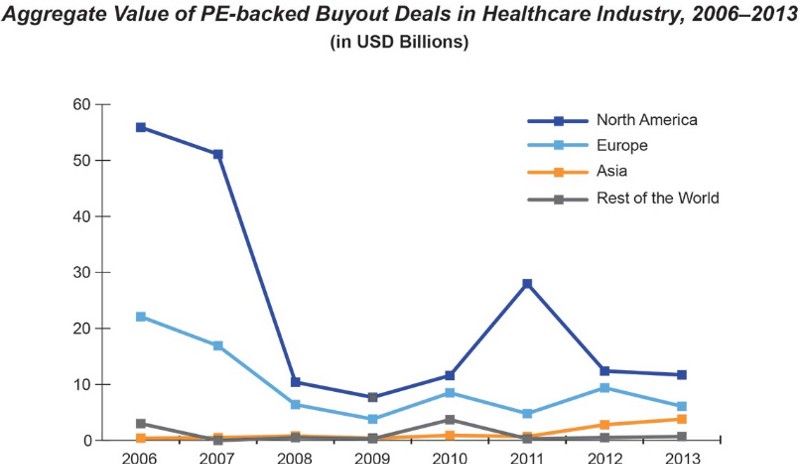

Healthcare buyout deals in Asia by PE funds have risen steadily since 2011. However, even with growth projections and trends being so favorable for the healthcare industry in Asia, overall M&A activity has continued to be heavily focused on the U.S.

Preqin

It is estimated that there are ~350 healthcare-specific funds based in the U.S., with only about 15 specialized health funds being operated out of emerging markets. One reason for this is that deal sizes and depth in emerging regions like Asia are considered insufficient for specialized funds. This has resulted in sector-agnostic funds taking on the opportunity to invest in healthcare opportunities in fast-growing emerging markets.

Given that healthcare companies and practices tend to be far more fragmented in Asia than in the U.S., deals are often at an earlier stage of the life cycle, and more likely to attract venture capital over PE funds. Indeed, over the past three years, more than 55% of all healthcare deal activity in Asia has been VC-backed. The fragmentation in the space also means, however, that there is far more opportunity for consolidation and buyouts. As the region’s healthcare market continues to mature, informed investors who understand which Asian countries and healthcare sub-sectors to focus on, at which time, will be able to benefit from this opportunity-laden investment environment.

There is ample potential for strategic players of all sizes to drive organic growth in Asia. Furthermore, there is scope for equity sponsors to back (or acquire) small, fast-growing companies individually or in combination (through consolidation), as distribution channels emerge and the entire ecosystem grows.

With the substantial growth and variability between markets and customer groups, the keys to success in Asia lie in understanding the nuances of markets, opportunities, and risks, and in determining where to build and invest in organic growth versus where to acquire and ride the wave of market growth on current infrastructure. The opportunities are significant. The question is how best to realize them.

Read More